New Energy World™

New Energy World™ embraces the whole energy industry as it connects and converges to address the decarbonisation challenge. It covers progress being made across the industry, from the dynamics under way to reduce emissions in oil and gas, through improvements to the efficiency of energy conversion and use, to cutting-edge initiatives in renewable and low-carbon technologies.

Li-ion BESS market set for growth, while new leasing deal promises to ‘unlock’ European sector

14/8/2024

News

Global demand for lithium-ion (Li-ion) battery-based energy storage systems (BESS) is projected to soar as renewable energy sources increasingly integrate into power grids worldwide. According to IDTechEx’s latest report, the market is expected to reach $109bn in value by 2035, with over 4.4 TWh installed worldwide, driven by government incentives, technological advancements and the rising need for grid stability. Meanwhile, a new long-term tolling agreement is looking to ‘unlock’ energy storage opportunities across Europe.

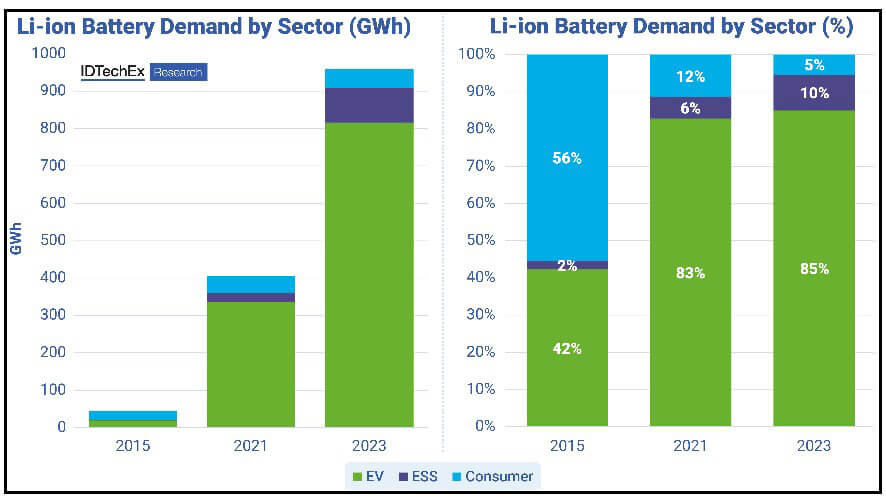

Li-ion batteries, which already dominate the energy storage landscape (accounting for over 90% of installations), are experiencing heightened demand across multiple sectors (see Fig 1). In 2023 alone, global demand for Li-ion batteries reached approximately 960 GWh, a significant jump from 400 GWh in 2021, according to IDTechEx’s latest sector report. While electric vehicle (EVs) accounted for the bulk of this demand, the BESS sector’s share increased to 10% in 2023, up from 6% in 2021 and just 2% in 2015.

Fig 1: Li-ion battery demand by sector

Source: IDTechEx

China and the US lead the global BESS market, responsible for 49% and 22% respectively of the 92.3 GWh of Li-ion BESS deployed in 2023, marking a fourfold increase since 2021. China’s dominance is partly due to aggressive domestic manufacturing and price competition, which has also spurred Chinese BESS companies to explore overseas markets for growth opportunities. This has sparked concern in Europe and the US, which are looking to protect their domestic manufacturing sectors through energy policies such as the European Net Zero Industry Act and the US Inflation Reduction Act, with tax and other incentives aimed at reducing production costs and enhancing competitiveness.

Beyond China and the US, other regions are gearing up for significant BESS expansion, with countries like the UK, Germany, Italy, Australia and India implementing policies to drive adoption of the technology. For example, Australia’s Capacity Investment Scheme targets 500 MW of ‘clean dispatchable energy’ in its first tender, while India plans to support up to 4 GWh of BESS deployment through its Viability Gap Funding initiative.

Li-ion technology continues to evolve, with a notable shift towards using lithium iron phosphate (LFP) cells over nickel manganese cobalt (NMC) cells in BESS applications, notes the report. LFP cells, favoured for their lower cost and longer cycle life, now dominate the Li-ion BESS market. However, they offer lower energy density compared to NMC cells, which has led to innovations such as the development of larger cell formats and containerised systems with capacities exceeding 5 MWh. These advancements increase energy density at the system level, reduce installation footprints and lower overall project costs, making high-capacity BESS more competitive in the market.

Looking ahead, while Li-ion BESS will likely maintain dominance in the near term, alternative technologies are emerging, reports IDTechEx. Materials like sodium-ion, redox flow and metal-air batteries offer potential advantages, particularly in terms of cost, safety and recyclability. However, these technologies are still in development, it adds.

New long-term tolling agreement for BESS to help ‘unlock’ European sector

In related news, Shell has signed a seven-year tolling agreement with global energy storage owner-operator BW ESS and its partner Penso Power for their 330MWh Bramley BESS currently under construction in Hampshire, UK. Bramley is expected to be the longest-duration BESS in the UK (3.3 hours) at the time of commissioning, which is expected in 4Q2024.

A tolling agreement provides a guaranteed, fixed-price revenue return for an asset. The deal is the first such for a single BESS asset in Great Britain, ‘creating a template for a new revenue structure that will help to unlock energy storage market opportunities across Europe’, report BW ESS and Penso Power.

Commenting on the deal, Erik Strømsø, CEO of BW ESS, says: ‘This tolling agreement… demonstrates the attractiveness of longer-duration, higher-performance battery systems. It not only secures long-term revenues for Bramley, but also helps enable the market’s shift away from short-term frequency response towards load shifting.’

The 100 MW/330 MWh Bramley site is the first project in Europe to deploy Sungrow’s PowerTitan 2.0 liquid cooled BESS – a system that combines a 2.5 MW power conversion system using integrated string inverters and a 5 MWh battery into a single container.

Earlier this year, Octopus Energy entered into a two-year toll agreement with Gresham House Energy Storage Fund (GRID) for half of its UK BESS portfolio, representing 568 MW/920 MWh of power. The deal, reported to be the first of its kind in the British energy market and the biggest in the world, aims to cut curtailment costs, which cost UK energy bill payers some £800mn in 2022.